44 risk of zero coupon bonds

Zero Coupon Bond -Features, benefits, drawbacks, taxability, & FAQs Interest Rate Risk: Zero-coupon bonds that are sold before maturity are subject to interest rates risk. This is because the value of these bonds is inversely proportional to interest rates. Hence, if interest rates rise, the value of these bonds declines in the secondary market. Yield to Maturity and Default Risk - Do Financial Blog 23. The stated yield to maturity and realized compound yield to maturity of a (default-free) zero-coupon bond will always be equal. Why? 24. Suppose that today's date is April 15. A bond with a 10% coupon paid semiannually every January 15 and July 15 is listed in The Wall Street Journal as selling at an ask price of 101:04. If you buy the bond ...

SGS Bonds: Information for Individuals Coupon Payment: Semi-annual coupon starting from the month of issue. Paid on the first business day of the month. Transferable: Yes. SGS bonds can be traded on the secondary market - at DBS, OCBC, or UOB branches; or on SGX through securities brokers. Maturity and redemption: No early redemption, but can be sold in the secondary market ...

Risk of zero coupon bonds

Zero-Coupon CDs: What They Are And How They Work | Bankrate You'll pay a discounted price for a zero-coupon CD in exchange for not being paid interest throughout the term. You'll receive the full face value of the CD, plus all the interest, once it matures.... What Are Treasury STRIPS? - Investment Guide - SmartAsset When stripping of Treasury bonds began, the government discouraged the practice due to concerns about lost tax revenues. However, in 1982 tax laws were modified to change tax treatment of zero-coupon bonds.The Treasury department then accepted stripping and also began issuing bonds electronically, without paper certificates or coupons. Zero-Coupon Bond - Definition, How It Works, Formula A zero-coupon bond is a bond that pays no interest. The bond trades at a discount to its face value. Reinvestment risk is not relevant for zero-coupon bonds, but interest rate risk is relevant for the bonds. Understanding Zero-Coupon Bonds As a zero-coupon bond does not pay periodic coupons, the bond trades at a discount to its face value.

Risk of zero coupon bonds. Coupon Rate - Learn How Coupon Rate Affects Bond Pricing Bonds that are rated "B" or lower are considered "speculative grade," and they carry a higher risk of default than investment-grade bonds. Zero-Coupon Bonds A zero-coupon bond is a bond without coupons, and its coupon rate is 0%. The issuer only pays an amount equal to the face value of the bond at the maturity date. Quant Bonds - Zero Volatility - BetterSolutions.com In this regard there is zero volatility. Example - Z Spread for a Corporate Bonds. Lets compare 2 different corporate bonds with the same maturity date but with different coupons Company B has a 10 year, 5% coupon bond The Z spread can be found using an iterative process Lets start with a spread of 100 basis points (or 1%) How to Invest in Bonds: A Beginner's Guide to Buying Bonds There are two ways to make money by investing in bonds. The first is to hold those bonds until their maturity date and collect interest payments on them. Bond interest is usually paid twice a year ... Philippines Government Bonds - Yields Curve The Philippines 10Y Government Bond has a 6.719% yield.. 10 Years vs 2 Years bond spread is 216.9 bp. Normal Convexity in Long-Term vs Short-Term Maturities. Central Bank Rate is 2.25% (last modification in May 2022).. The Philippines credit rating is BBB+, according to Standard & Poor's agency.. Current 5-Years Credit Default Swap quotation is 57.35 and implied probability of default is 0.96%.

How Do Interest Rate Risk and Reinvestment Risk Interact? Zero coupon bonds are one way to manage reinvestment risk. These bonds don't make periodic interest payments. Investors only have to think about investing at face value. Zero coupon bonds are sold at a discount price because of the date discounts on their face value. Investors can also invest in non-callable bonds. 5 Year Treasury Rate - YCharts The 5 year treasury yield is included on the longer end of the yield curve. Historically, the 5 Year treasury yield reached as high as 16.27% in 1981, as the Federal Reserve was aggressively raising benchmark rates in an effort to contain inflation. 5 Year Treasury Rate is at 3.25%, compared to 3.07% the previous market day and 0.73% last year. Basics Of Bonds - Maturity, Coupons And Yield To calculate the current yield for a bond with a coupon yield of 4.5 percent trading at 103 ($1,030), divide 4.5 by 103 and multiply the total by 100. You get a current yield of 4.37 percent. Say you check the bond's price later and it's trading at 101 ($1,010). The current yield has changed. Divide 4.5 by the new price, 101. US Treasury Zero-Coupon Yield Curve - NASDAQ Refreshed 2 days ago, on 17 Jun 2022 ; Frequency daily; Description These yield curves are an off-the-run Treasury yield curve based on a large set of outstanding Treasury notes and bonds, and are based on a continuous compounding convention. Values are daily estimates of the yield curve from 1961 for the entire maturity range spanned by outstanding Treasury securities.

What Is a Zero Coupon Yield Curve? (with picture) A zero coupon bond does not pay interest but instead carries a discount to its face value. The investor therefore receives one payment of the face value of the bond on its maturity. This face value is the equivalent of the principal invested plus interest over the life of the bond. Interest Rate Risk: Definition, Formula & Models - Study.com Zero coupon bonds are a form of bond that makes no interest payment and pays back its face (par) value at maturity. If we assume that a zero-coupon bond with a par value of $1,000 that matures in... Deferred Coupon Bonds | Definition, How it works? Types, Advantages Deferred coupon bonds can be Zero-coupon bonds for a specific period of time and then pay a certain interest for the remaining period till maturity. For example, a deferred coupon bond with 4 years as a deferred period with a coupon of 6% will not pay any interest for the first four years from the issuance date. Brazil Government Bonds - Yields Curve The term credit default swap (CDS) refers to a financial derivative that allows an investor to swap or offset their credit risk with that of another investor. To swap the risk of default, the lender buys a CDS from another investor who agrees to reimburse the lender in the case the borrower defaults.

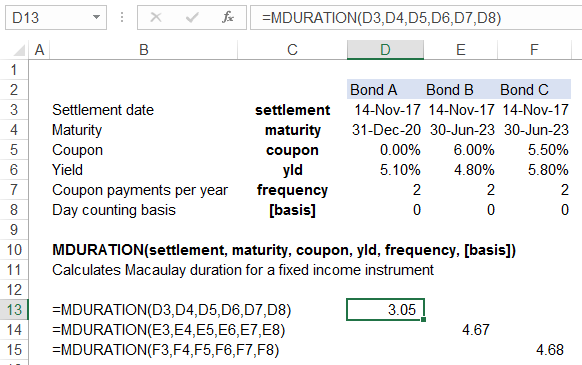

Bond Duration | Formula | Excel | Example

Zero-Coupon Bond Definition - Investopedia Zero-coupon bonds are like other bonds, in that they do carry various types of risk, because they are subject to interest rate risk if investors sell them before maturity. How Does a Zero-Coupon...

Post a Comment for "44 risk of zero coupon bonds"